Report: How economic pressure is reshaping consumer spending

A new report from Prolific and Checkbox shows a consumer population that’s careful with money, disciplined about spending, and more shaped by economic pressure than by brand influence.

You may not be surprised. After years of inflationary pressure and economic uncertainty, caution has become part of the consumer landscape.

Across North America and Northern Europe, consumers often behave in remarkably similar ways. They budget, they think twice before spending, and they prioritize essentials.

In fact, according to McKinsey’s State of the Consumer 2025 report, one-third of consumers made savings in one area to invest more in another:

“Cross-category trade-downs—trading down in one category to afford something in another—are becoming more prevalent.”

Underneath those shared habits, the report found meaningful differences in financial anxiety, future optimism, and payment behavior.

Caution is not a niche behavior

The most striking finding in our report is how little spending priorities varied across age groups and regions.

Across North America and Northern Europe, consumers clustered around the same three purchasing strategies:

- 47% prefer fewer, higher-quality items

- 27% take more time before making purchases

- 26% choose cheaper alternatives where possible

Statistical testing found no significant effect of region or age on those purchasing priorities.

That challenges a familiar assumption in consumer research: that spending caution belongs to a particular generation, region, or life stage.

The report suggests something different: Cautious, quality-oriented consumption looks to be a broad response to the current economic environment, rather than a clean demographic segment. In other words, cautious consumers have become the baseline.

Similar behavior can hide different experiences

Shared behavior doesn’t mean shared experience.

The report found that spending habits across North America and Northern Europe were broadly similar, but financial worry was not.

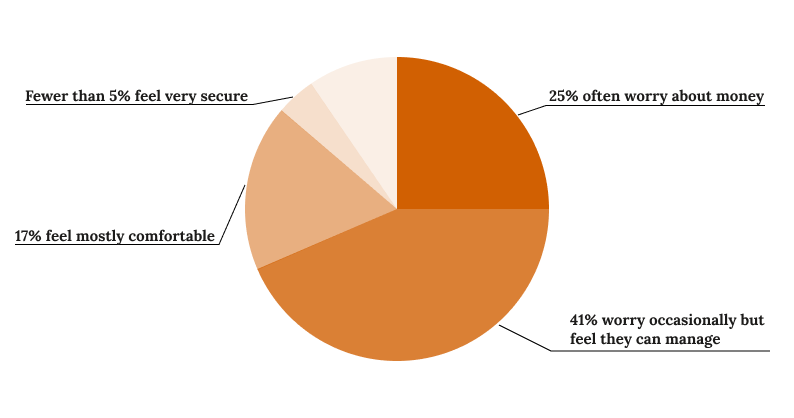

Around 34% of North American respondents said they often worry about money, compared with around 18% in Northern Europe. Across the full sample:

- 25% often worry about money

- 41% worry occasionally but feel they can manage

- 17% feel mostly comfortable

- Fewer than 5% feel very secure.

For example, two consumers may both delay a purchase; one is making a calm, value-conscious decision, while the other is managing acute financial pressure. The observable behavior is the same, but the emotional and economic context is not.

Age still matters, but not everywhere

When it came to financial optimism, age was a stronger signal than geography.

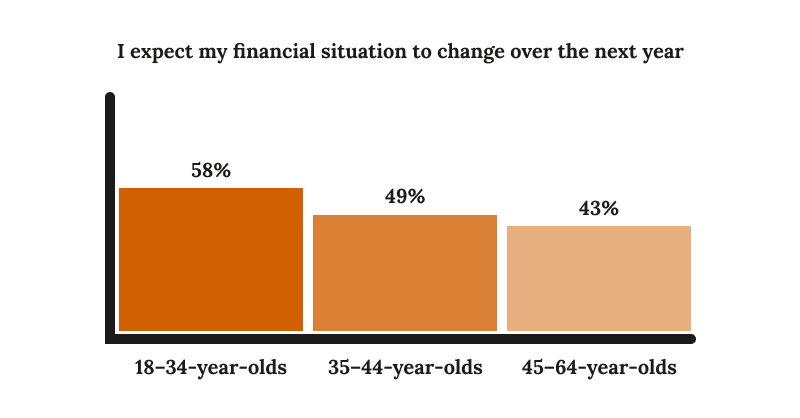

When asked whether they expected their financial situation to change over the next year, younger consumers were more likely to anticipate change.

Around 58% of 18–34-year-olds expected their finances to change, compared with around 49% of 35–44-year-olds and 43% of 45–64-year-olds.

Younger consumers may not be more financially secure, but they appear more likely to expect a change in their financial situation.

Region still has an impact, however – as mentioned, the report found that North America carries a higher burden of financial anxiety, while payment behavior also differs by region and generation.

Local context still has an impact on payment behavior

Payment methods were one area where regional and generational differences remained clear.

- Credit card usage was significantly higher in North America

- Mobile payment adoption, including Apple Pay and Google Pay, varied significantly by both region and age, with younger consumers showing higher adoption

- Cash and debit card usage showed no significant variation by age or region

That mix of change and stability shows that even when consumers have access to innovative fintech, they still sometimes rely on familiar payment behaviors.

The biggest spending driver isn’t brand

People’s spending decisions were shaped more by economic pressure – rising prices, job stability, exchange rates, and household costs – than by brand reputation or recommendations from friends and family.

Although it doesn’t mean that it’s irrelevant, the data suggests that brand becomes a consideration for consumers only once they have decided how to budget and allocate their spending.

What this means for research teams

Our report is a strong example of what thoughtful survey design can reveal.

The value is not just in asking consumers what they buy or how they feel about brands. It’s in building studies that capture the economic and emotional context around those answers.

For consumer researchers, that means adding variables that help explain constraint:

- Inflation exposure

- Job security sentiment

- Household financial obligations

- Financial confidence

- Perceived control over money

- Decision stage: whether someone is deciding to spend, or deciding what to buy

A person’s age may help explain financial optimism, their region may help explain payment behavior or financial anxiety, and their attitude toward a brand may help explain product preference.

Conclusion

The report from Prolific and Checkbox paints a picture of consumers who are cautious by default. They’re budgeting, prioritizing essentials, and making spending decisions in an environment where economic pressure carries real weight.

Contact us

Fill out this form and our team will respond to connect.

If you are a current Checkbox customer in need of support, please email us at support@checkbox.com for assistance.